Filing income tax returns (ITR) in India often brings up complex questions about maximizing deductions, especially when caring for family members. Sections 80D and 80DD of the Income Tax Act offer significant financial relief for healthcare-related costs. However, understanding when you need physical proof, what limits apply, and how the tax regimes affect your claims is crucial to avoiding rejections or penalties.

Section 80D: Medical Insurance and Expenditures

A Health policy is a legal contract between you and your insurer that defines the scope of medical expenses it will cover, the sum insured available, applicable waiting periods, and the terms under which a claim can be made. Reading and understanding your Health policy document carefully before purchase helps you avoid unpleasant surprises at the time of hospitalisation, particularly around exclusions for specific conditions or treatments. Star Health’s Health policy documents are written in plain language, with clearly defined coverage terms, pre-existing disease waiting periods, and network hospital lists that make it straightforward for policyholders to understand what they are buying. Renewing your Health policy before the due date protects the continuity benefits you have earned, including reduction in waiting periods and any no-claim bonus accumulated over prior years. A well-chosen Health policy remains one of the most cost-effective ways to manage the financial risk that comes with unexpected medical events.

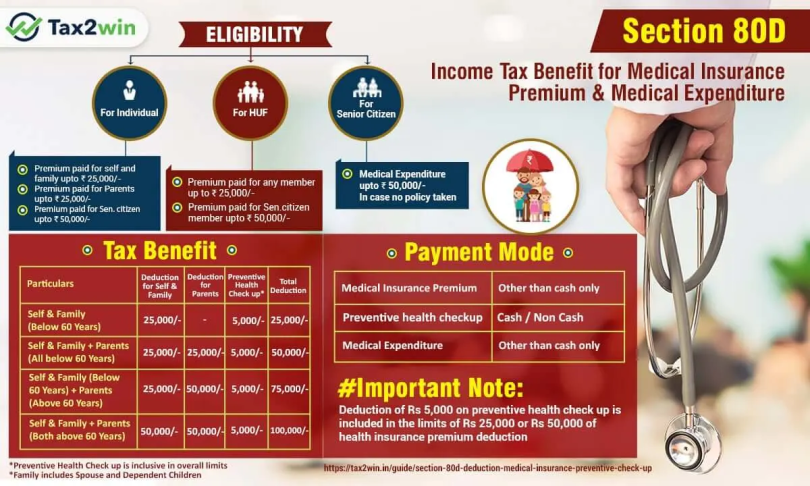

Section 80D allows individuals and Hindu Undivided Families (HUFs) to claim tax benefits on health insurance premiums, preventive health check-ups, and actual medical expenditures.

Do You Need Proof to Claim Section 80D?

The quick answer is no, you do not need to upload proof when filing your ITR. The Income Tax Department does not mandate attaching receipts or policy documents on the e-filing portal. However, retaining proof is mandatory for two reasons:

Employer Verification: Salaried employees must submit receipts to their employer so the deduction can be reflected in Form 16.

Tax Department Scrutiny: If your file is selected for audit or verification later, failing to produce valid documents can result in severe penalties and the reversal of tax benefits.

Premium Payments vs. Uninsured Medical Expenses

The necessity of actual medical bills varies depending on what you are claiming:

Health Insurance Premiums: No medical bills are needed. You only need the insurance company’s payment receipt. Crucial Rule: Except for preventive health check-ups, payments made in cash are not allowed for deductions. Premiums must be paid via non-cash modes (e.g., net banking, debit/credit cards, UPI, or cheques).

Medical Expenditure for Senior Citizens: If your senior citizen parents (aged 60 or above) do not have health insurance coverage, you can claim their actual medical expenditures (medicines, doctor visits, diagnostic tests). In this scenario, actual bills and prescriptions are strictly required as proof of spending.

Table: Section 80D Rules At-A-Glance

Maximum Cumulative Deduction: If both the taxpayer and their parents are senior citizens, the total cumulative deduction available under Section 80D can reach up to ₹1,00,000 per financial year.

Section 80DD: Maintenance of a Disabled Dependent

Section 80DD provides fixed tax deductions to resident individuals and HUFs who look after a dependent family member with a disability. Eligible dependents include a spouse, children, parents, or siblings who rely financially on the taxpayer.

The Tax Regime Restriction

Unlike Section 80D, deductions under Section 80DD are only available under the old tax regime. Taxpayers opting for the simplified new tax regime cannot claim this benefit.

Fixed Deduction Amounts

The deduction amount under Section 80DD is fixed based on the severity of the disability and does not depend on your actual out-of-pocket expenses:

Standard Disability (40% to 79%): A flat deduction of ₹75,000.

Severe Disability (80% or more): A flat deduction of ₹1,25,000.

Mandatory Documentation for Section 80DD

You cannot claim an 80DD deduction without official documentation. While you do not upload them during filing, you must keep them on file to prevent claim rejection or disputes:

Authorized Medical Certificate: A compulsory certificate clearly stating the type and percentage of disability. It must be issued by a recognized government specialist, such as a civil surgeon or neurologist.

Form 10-IA: This form must be completed and certified by a medical specialist for severe or complex conditions like autism, cerebral palsy, or multiple disabilities.

Self-Declaration Certificate: A signed statement from the taxpayer confirming they handle the medical treatment, training, rehabilitation, or maintenance of the dependent.

Insurance Premium Receipts: If you have invested in specific approved insurance schemes meant for the rehabilitation of the disabled dependent, preserve those premium receipts.

Summary Checklist for Taxpayers

To safeguard your health deductions against future scrutiny, ensure you maintain an organized digital or physical folder containing:

Insurance policy documents and non-cash premium receipts.

Doctor consultation prescriptions and hospital admission details.

Original pharmacy invoices, bills, and official diagnostic/laboratory test results (X-rays, scans).

Valid disability certificates and certified official tax forms (like Form 10-IA) if claiming under the old tax regime for disabled dependents.

Individual health insurance is designed to provide dedicated medical coverage to a single policyholder, ensuring the entire sum insured is available for that person alone without being shared with family members. This is particularly valuable for working adults with specific health conditions, frequent travellers, or anyone whose medical needs differ significantly from those of their family. Individual health insurance from Star Health includes coverage for hospitalisation, surgical procedures, pre- and post-hospitalisation expenses, and optional add-ons like critical illness cover, personal accident protection, and OPD benefits. Buying individual health insurance at a young age locks in lower premiums before lifestyle or age-related health conditions emerge, allowing a longer track record for no-claim bonuses to build. Reviewing your individual health insurance plan every few years helps ensure the sum insured and add-ons remain aligned with your current health profile and financial goals.